The U.S. Department of the Treasury and the IRS on Dec. 22, 2023, released proposed regulations regarding the production tax credit (PTC) for hydrogen under Section 45V of the Internal Revenue Code, as enacted by the Inflation Reduction Act. Comments to the proposed regulations are due on Feb. 26, 2023. In conjunction with the proposed regulations, the U.S. Department of Energy (DOE) also released a whitepaper and the updated version of the Greenhouse Gases, Regulated Emissions, and Energy Use in Transportation (GREET) model applicable to clean hydrogen production, named 45VH2-GREET 2023. Finally, the U.S. Environmental Protection Agency (EPA) also weighed in, providing a letter to the Treasury Department to inform some of the interpretations it made in the proposed regulations.

Under Section 45V, a PTC is available for each kilogram of clean hydrogen produced during the taxable year for the first 10 years after the hydrogen generation facility is placed into service at an amount of up to $3 (adjusted for inflation) per kilogram of hydrogen depending on the carbon intensity of the hydrogen. Taxpayers may elect to claim the investment tax credit (ITC) under Section 48 in lieu of the Section 45V PTC.

This Holland & Knight alert breaks down the highlights of the proposed regulations. The exact implications of these rules depend on particular sets of facts.

Clean Hydrogen Production Facility

The proposed regulations provide that a clean hydrogen production facility means a single production line that is used to produce qualified clean hydrogen. A single production line includes all components of property that function interdependently to produce qualified clean hydrogen. Components of property function interdependently to produce qualified clean hydrogen if the placing in service of each component is dependent upon the placing in service of each of the other components to produce qualified clean hydrogen.

The facility does not include equipment that is used to condition or transport hydrogen beyond the point of production or electricity production equipment used to power the hydrogen production process (the latter including any carbon capture equipment associated with the electricity production process).

Coordination with Section 45Q Credit

Prop. Treas. Reg. § 1.45V-2(a) provides that if a qualified clean hydrogen production facility includes carbon capture equipment for which a credit is allowed to any taxpayer under Section 45Q for the taxable year or any prior taxable year, no Section 45V credit is allowed for the production of qualified clean hydrogen for that taxable year.

However, if the 80/20 Rule, discussed below and provided in Treas. Reg. § 1.45Q-2(g)(5), is satisfied with respect to such carbon capture equipment and no new Section 45Q credit has been allowed to any taxpayer for such carbon capture equipment, then the unit of carbon capture equipment for which the 80/20 Rule is satisfied will not be treated as carbon capture equipment for which a Section 45Q credit was previously allowed, thus not blocking the taxpayer from claiming Section 45V.

Anti-Abuse Rule

The proposed regulations include an anti-abuse rule and disallow the credit under Section 45V if the primary purpose of the production and sale or use of qualified clean hydrogen is to obtain the benefit of the Section 45V credit in a manner that is wasteful, such as the production of qualified clean hydrogen that the taxpayer knows or has reason to know will be vented, flared or used to produce hydrogen.

GREET Model Used to Define Life-Cycle Greenhouse Gas Emissions Rates

The proposed regulations provide that the amount of the Section 45V credit is determined by reference to the life-cycle greenhouse gas (LGHG) emissions rate of all hydrogen produced at a qualified clean hydrogen production facility during a taxable year. That is, taxpayers claiming the Section 45V credit must determine the applicable LGHG emissions rate provided in the most recent GREET Model separately for each facility.

The proposed regulations generally define the most recent GREET Model as the latest version of the model that is publicly available on the first day of the taxable year during which the qualified clean hydrogen for which the taxpayer is claiming the Section 45V credit is produced. In the event the most recent GREET Model does not provide a LGHG emissions rate associated with a facility's hydrogen production pathway (this is if either the feedstock used by the facility or the production technology is not included in the most recent GREET model), the proposed regulations include detailed procedures for taxpayers to petition for a provisional emissions rate (PER). The announced 45VH2 GREET 2023 includes the following hydrogen production pathways:

- steam methane reforming (SMR) of natural gas with potential carbon capture and sequestration (CCS)

- autothermal reforming (ATR) of natural gas with potential CCS

- SMR of landfill gas with potential CCS

- ATR of landfill gas with potential CCS

- coal gasification with potential CCS

- biomass gasification with potential CCS

- low-temperature water electrolysis using electricity

- high-temperature water electrolysis using electricity and/or heat from nuclear power plants

If a PER petition is approved, a taxpayer can rely on the PER until such time as a LGHG emissions rate for the particular hydrogen production pathway is provided in the most recent GREET Model.

Energy Attribute Certificates for Hydrogen Produced Using Grid-Connected Electricity

Under the proposed regulations, taxpayers are able to treat a hydrogen production facility's use of grid-connected electricity as being from a specific electricity generation facility (or facilities) only if the taxpayer acquires and retires qualifying energy attribute certificates (EACs) for each unit of electricity that the taxpayer claims from such source. EACs are tradeable contractual instruments, issued through a qualified EAC registry or accounting system, that represent the energy attributes of a specific unit of energy produced. Renewable energy certificates (RECs) and other similar energy certificates issued through a registry or accounting system are forms of EACs.

EACs are "qualifying EACs" only if they satisfy the following three requirements (commonly referred to as the "three pillars") for "eligible EACs" and such requirements are verified by a qualified verifier (discussed further below under Prop. Treas. Reg. § 1.45V-5).

Incrementality

Incrementality generally requires that the EACs represent incremental or additional sources of electricity from clean power generation that began commercial operations no more than 36 months prior to the date the hydrogen facility was placed in service or the generating facility had an uprate (i.e., an increase in its rated nameplate capacity in nameplate megawatts) within such timeframe.

Temporal Matching

Temporal matching generally requires that the electricity represented in the EAC be generated in the same hour that the taxpayer's hydrogen production facility uses electricity to produce hydrogen.

The proposed regulations include a "transition rule" for EACs that represent electricity generated prior to Jan. 1, 2028. Such electricity would be subject to a yearly rather than an hourly matching requirement.

Deliverability

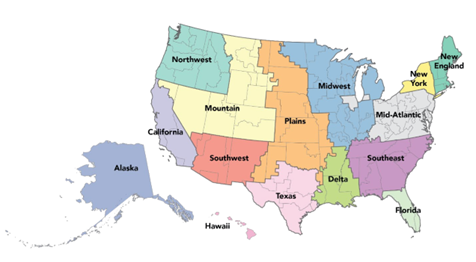

Deliverability generally requires that the electricity represented in the EAC be sourced from the same region as the taxpayer's hydrogen production facility.

For these purposes, the term "region" means a region derived from the National Transmission Needs Study issued by the DOE on Oct. 30, 2023. Such regions are depicted below; note that each U.S. territory is treated as a separate region.

Source: U.S. Department of Energy

Renewable Natural Gas and Fugitive Sources of Methane

The proposed regulations do not provide rules regarding the use of renewable natural gas (RNG) and fugitive sources of methane1 to produce hydrogen. The preamble notes that the Treasury Department and IRS anticipate requiring that for biogas or biogas-based RNG to receive an emissions value consistent with that gas (and not standard natural gas), the RNG used during the hydrogen production process must originate from the first productive use of the relevant methane. Productive use is generally defined as any valuable application of biogas, including to provide heat or cooling, generate electricity or upgrade to RNG and not venting or flaring. The Treasury Department and IRS propose to define "first productive use" of methane as the time when a producer of that gas first begins using or selling it for productive use in the same taxable year as (or after) the relevant hydrogen production facility was placed in service.

Modification of an Existing Hydrogen Facility

Prop. Treas. Reg. § 1.45V-6(a)(1) provides that in the case of an existing facility placed in service prior to 2023 (i.e., prior to the effective date of Section 45V) that was not capable of producing clean hydrogen, but that undergoes a modification to produce clean hydrogen, such facility will be considered to have been placed in service after such modification. For this rule to apply, amounts paid or incurred with respect to such modification must be properly chargeable to the taxpayer's capital account for the facility. Finally, with respect to such existing facilities that produced hydrogen, a modification is made if the facility could not, as it existed, produce clean hydrogen (i.e., hydrogen with a LGHG emissions rate that is less than or equal to 4 kilograms of CO2e).2

The 80/20 Rule

In addition to the modification rule, the proposed regulations also adopt the traditional 80/20 Rule, which allows a previously placed-in-service facility to be considered a "new" facility for purposes of Section 45V, where the fair market value (FMV) of the existing components of the "old" facility make up no more than 20 percent of the FMV of the "new facility." If a facility satisfies the 80/20 Rule, then the date on which such facility is considered originally placed in service for purposes of Section 45V is the date on which the new property added to the facility is placed in service.

Verification Requirements

The proposed regulations provide that in order to claim the Section 45V credit, a taxpayer must attach a verification report, prepared by a qualified verifier under penalties of perjury, to Form 7210, for each facility and year for which the taxpayer claims the credit. The verification report must contain the following items:

- Production Attestation. The verification report must specify and attest that the following data is correct: the amount of hydrogen claimed for credit, the GREET data or the PER data; the emissions value received from the DOE if a PER was used, the LGHG emissions rate (expressed in kilograms of CO2e per kilogram of hydrogen) and the amount of qualified clean hydrogen produced by the taxpayer (expressed in kilograms).

- Sale or Use Attestation. The verification report must attest "verifiable use" of the hydrogen. Verifiable use can occur inside or outside the U.S. and includes tolling arrangements. Verifiable use does not include 1) use of hydrogen to generate electricity that is then directly or indirectly used in the production of additional hydrogen or 2) venting or flaring of hydrogen.

- Conflict Attestation. The verification report must attest that the verifier has no conflict of interest. If a Section 6418 transfer election is being made, then the verifier must attest its independence from both the eligible taxpayer and the transferee taxpayer.

- Qualified Verifier Statement. The verification report must include the verifier's Taxpayer Identification Number (TIN) and document the verifier's qualifications. A verifier can either be qualified by the American National Standards Institute National Accreditation Board or the California Air Resources Board Low Carbon Fuel Standard

- General Information About the Hydrogen Production Facility. The verification report must also discuss the method of producing the hydrogen, discuss the type(s) and amount(s) of feedstock used, list the metering devices used, and attest that the metering devices were calibrated and tested for accuracy in the last year.

- Necessary Documentation. The verification report must contain any documentation necessary to substantiate the verification process given the standards and best practices prescribed by the verifier's accrediting body and the circumstances of the taxpayer and the taxpayer's hydrogen production facility.

The verifier must sign and date the verification report by the due date or extended due date of the tax return or information return for the taxable year during which the hydrogen undergoing verification is produced. When a credit is first claimed on an amended return or administrative adjustment request, the report is due on the day the amended return or administrative adjustment request is filed.

The proposed regulations provide that if a taxpayer produced electricity for which either the Section 45 or Section 45U credit is claimed and also used that electricity to produce qualified clean hydrogen, the verification report must attest that 1) the electricity used to produce such hydrogen was produced at the relevant facility for which a Section 45 or Section 45U credit is claimed, 2) the given amount of electricity (in kilowatt hours) used to produce such hydrogen at the relevant hydrogen production facility is reasonably assured of being accurate and 3) the electricity for which a Section 45 or 45U credit was claimed is represented by EACs that are retired in connection with the production of such hydrogen.

Notes

1 Fugitive methane refers to the release of methane through, for example, equipment leaks or venting during the extraction, processing, transformation and delivery of fossil fuels to the point of final use, such as coal mine methane or coal bed methane.

2 Prop. Treas. Reg. §1.45V-6(a)(2).