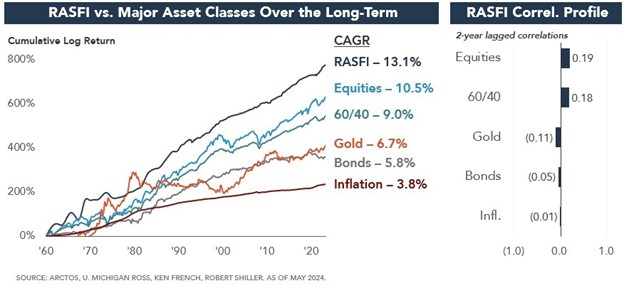

There was a time when ownership of a professional sports franchise was not regarded as a serious business venture. Owning a team, even in one of the major leagues in North America, was regarded as more of a frolic and detour, a cool thing to do if you had the money. No more—professional sports have become very serious business and returns on team investments can rival or exceed the returns from traditional asset classes. The recently developed Ross-Arctos Sports Franchise Index (RAFSI) measures the returns of team investments in the four major leagues in North America (MLB, NFL, NBA and NHL):

North American professional sports franchises in the Big Five leagues (NFL, NBA, MLB, NHL and MLS) were worth an average of nearly $3.2 billion in 2023. One of the most recent transactions in the NFL (the acquisition of the Washington Commanders) was valued at more than $6 billion and NFL clubs are reported to have average valuations that now approach or exceed $5 billion. The growth in NFL valuations has outpaced the S&P 500 over the past 20 years.1

The exceptional growth in professional sports valuations has been driven by dramatic increases in league media revenues. For example, the NBA’s new $76 billion suite of national media deals generates an average annual value (AAV) that represents a 2.6x increase over the previous national packages and could generate an average of nearly $200 million per team, beginning in the 2025-2026 season.

Against this backdrop of spiraling team valuations and unprecedented demand for sports-connected assets, leagues have been turning to institutional investors as important sources of capital and liquidity. The NBA, NHL, MLS and MLB have developed and implemented guidelines for private equity investments and the NFL has just announced that it will now follow suit and allow institutional investments. Key elements of the just-announced NFL policy:

- Teams may sell up to 10% of their common equity to league-approved institutional investors; the minimum deal size is 3%.

- Such investments will not convey governance rights nor is preferred equity allowed.

- Investments are subject to a six-year minimum holding period.

- No fund can invest in more than six teams.

- Funds must have committed capital of $2 billion and no team interest can account for more than 20% of a fund’s assets.

Private equity investments in sports have become increasingly commonplace as private equity firms, sovereign wealth funds and other asset managers have acquired interests in a number of NBA, MLB, NHL, MLS and NWSL clubs. In addition, private credit is beginning to play an increasingly important role in league and team financing. The rules governing such investments vary from league-to-league.

National Basketball Association

NBA franchise valuations have sky-rocketed over the last decade, driven by the League’s very valuable media rights and burgeoning international interest. Between 2010 and 2013, a number of NBA teams changed hands and the prices ranged from $350 million to $550 million. According to Sportico, in 2024, the average NBA team is now valued at nearly $4 billion. That’s way beyond Unicorn status.

The NBA’s ownership rules provide for institutional investments in teams. Private equity funds are permitted to hold up to a 20% stake in any franchise and each individual fund is limited to holding interests in a maximum of five franchises. The NBA also requires that any fund holding team interests have at least $750 million in assets and any team investment may not account for more than 25% of the applicable fund’s assets (though the NBA has flexibility to grant exceptions). The NBA also limits team owners from selling more than 30% of team equity to institutional investors.

Although the NBA once prohibited investments by governmental or quasi-governmental authorities and sovereign wealth funds, the League granted an exception to allow the Qatar Investment Authority (QIA) to acquire a minority, passive stake in Monumental Sports & Entertainment.

National Women's Soccer League

The NWSL has seen rapidly increasing team valuations, driven by the tidal wave of interest in women’s sports. For example, Angel City FC recently sold a controlling stake that valued the team at more than $250 million. The NWSL has always seen institutional investment as a key part of their growth strategy and private equity firms are not limited to minority investments in teams—Bay FC is owned by Sixth Street. The NWSL allows institutional investors to acquire minority stakes in up to three franchises, with ownership limited to between 5-20% of each club’s equity. Clubs may not sell more than 30% of their equity to institutional investors, and investing funds must have capital commitments of at least $100 million and must hold the investment for a minimum of five years. As with other leagues, all transactions (acquisitions and exits) are subject to league approval and must provide the club’s controlling owner with a right of first purchase. This requirement is like one that governs club transactions in MLS.2 At present, the NWSL does not allow investments from governmental or quasi-governmental entities.3

Major League Baseball

MLB became the first North American professional sports league to allow for institutional investment in 2019. MLB ownership rules cap limits private equity investors to 30% of any club’s equity, and a single fund may hold up to 15% of a team. Funds are not limited in the number of teams they may invest in, but investments in multiple teams are subject to a minimum five-year holding period.

National Hockey League

The NHL’s rules on institutional ownership permit clubs to sell up to 30% of their equity to institutional investors. Institutional investors may hold up to 20% of a maximum of five franchises (with each investment subject to a $20 million minimum). NHL institutional investments are also subject to a blanket minimum five-year holding period. The NHL does not allow active players to invest in teams, or in funds that invest in teams.4

Major League Soccer

MLS institutional investment rules are like those in other leagues, but also impose additional fund diversity requirements for “qualified fund[s]”.5 Similar rules include a four-team limit per fund, a $20 million minimum investment per team, a 20% investment limit in each franchise and an aggregate institutional ownership limit of 30% per franchise. For a private equity fund to be “qualified” to invest in the league, it must have at least $500 million in committed capital and not have concentrated ownership. A single investor or group may hold no more than 25% of such fund, may not invest more than 10% of the fund’s capital into a single franchise and may not concentrate more than 25% of the fund’s capital in MLS club investments.6 Asset managers may invest in common equity or senior equity instruments without debt-like features. Like other leagues, all investments in MLS clubs must be passive and carry limited governance rights. The club’s controlling owner must also have first negotiation rights upon the institutional investor’s exit and drag-along rights if they choose to sell their majority stake.

Takeaways

The demand for sports-connected assets has never been greater and marked increases in media revenues have been driving team and league valuations to even higher levels. While this is generally very good news for team owners and investors, rapidly rising valuations, coupled with strict league debt policies, create a need for institutional investment and capital. Jerry Jones bought the Dallas Cowboys in 1989 for $140 million; it’s hard to imagine completing such a large transaction today without institutional investment partners.

Private equity investments or private credit solutions can offer a unique solution for team owners seeking to augment limited liquidity for operations or to generate capital for technology investments or venue improvements. Institutional investors have become increasingly important partners in team ownership and the capital they provide fuels future growth for the leagues and continued growth in team valuations.

For institutional investors, there are key considerations. First, there are substantial differences in team operating parameters, with media market size being one of the most significant. As the regional sports network landscape continues to evolve, some teams in the NHL, NBA and MLB are seeing potentially significant reductions in local media rights revenue. While these reductions are largely offset by increases in national revenues at the NBA and MLB, that is not the case for all leagues. Teams in smaller media markets have more limited options for the distribution of local media rights, and agreements with over-the-air broadcasters generate a fraction of the revenue that Regional Sports Network (RSN) deals used to provide for teams,

Another complicating factor for institutional investors is the typical holding period for team and league investments. While several of the leagues impose explicit minimum holding periods, a more significant factor is the liquidity in the market. The limited number of team transactions each year, coupled with relatively long holding periods for these investments, make exits for institutional investors more challenging. Thoughtful and creative exit strategies need to be considered and negotiated when private equity investors close on investments in this space. Regardless, the enviable rates of growth in team valuations have more than made up for the liquidity challenges.

The NFL’s announcement of its institutional investment policy may well set off an old-fashioned land grab—with private equity and credit investors looking for pieces of not only some of the most iconic sports assets and brands in North America, but some of the most valuable and profitable teams in all of sports. The NFL’s decision to allow teams to seek investments of up to 10% from institutional investors could generate $12-$15 billion in transactions.

Long gone are the days when team ownership was regarded as a sideline hobby or a small family business. Today, sports teams are sophisticated media entities with multibillion-dollar valuations, generating returns that have been substantially out-performing other asset classes as investments and a need for the capital solutions provided by institutional investors. The trends driving these dramatic increases in team valuations and the just announced changes in the NFL's private equity policies may well unleash another torrent of investments in sports teams.

1 https://finance.yahoo.com/quote/%5EGSPC/history?period1=946684800&period2=1719187200&interval=1mo&filter=history&frequency=1mo&includeAdjustedClose=true

2 https://www.espn.com/nfl/story/_/id/40164039/private-equity-nfl-ownership-proposal-changes

3 https://www.sportico.com/business/team-sales/2024/nwsl-private-equity-rules-sovereign-wealth-1234768705/

4 https://www.espn.com/nfl/story/_/id/40164039/private-equity-nfl-ownership-proposal-changes

5 https://www.sportico.com/business/finance/2021/mls-private-equity-rules-1234645955/

6 https://www.sportico.com/business/finance/2021/mls-private-equity-rules-1234645955/