This year is starting to feel a bit more normalized after the 2021-2022 record origination numbers followed by the 2023 market disruption. In many ways, Fund finance has passed the stress test and moved forward. What has 2024 shown us through the first half?

Funds Market and the Demand for Credit

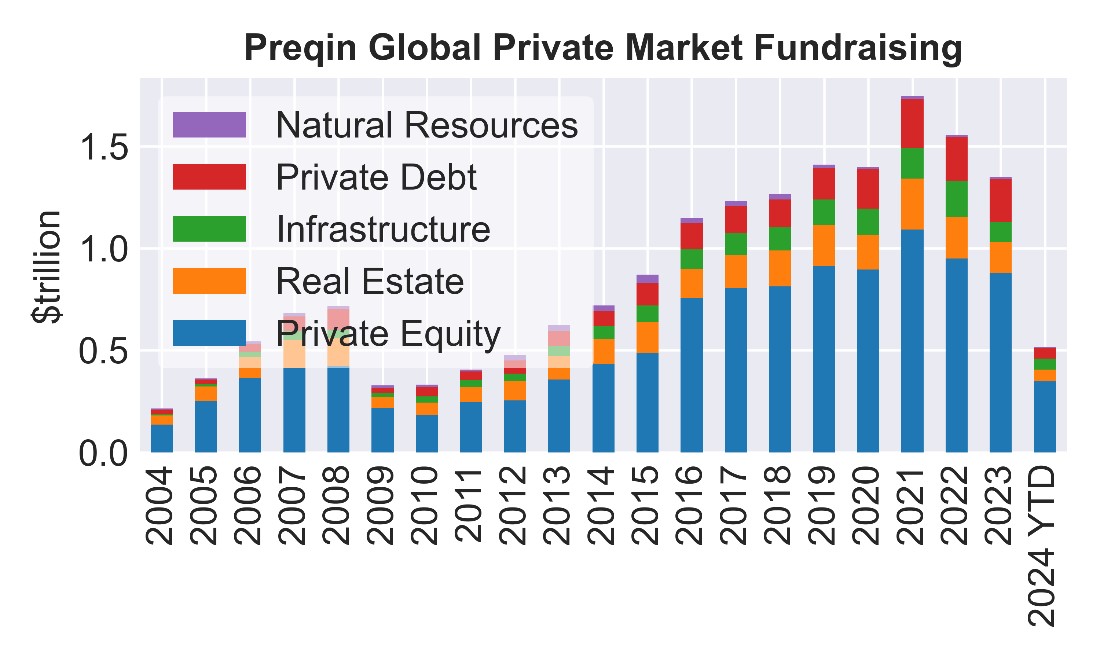

Source: Prequin.

- YTD fundraising of $514 billion looks roughly in line with last year’s pace and on track toward $1.2–1.4 trillion for the year.

- Consistent with our view coming into the year, we expect to see accommodative financial conditions (e.g., tight credit spreads, buoyant equity valuations, low volatility, contained credit, accommodative leverage) to drive improved private market capital velocity and support fundraising.

- We see a number of indications that this view is playing out as expected. Private credit lending volume, which primarily finances sponsor-owned companies, suggests deal activity will show sequential improvement when 1H PE data is reported.

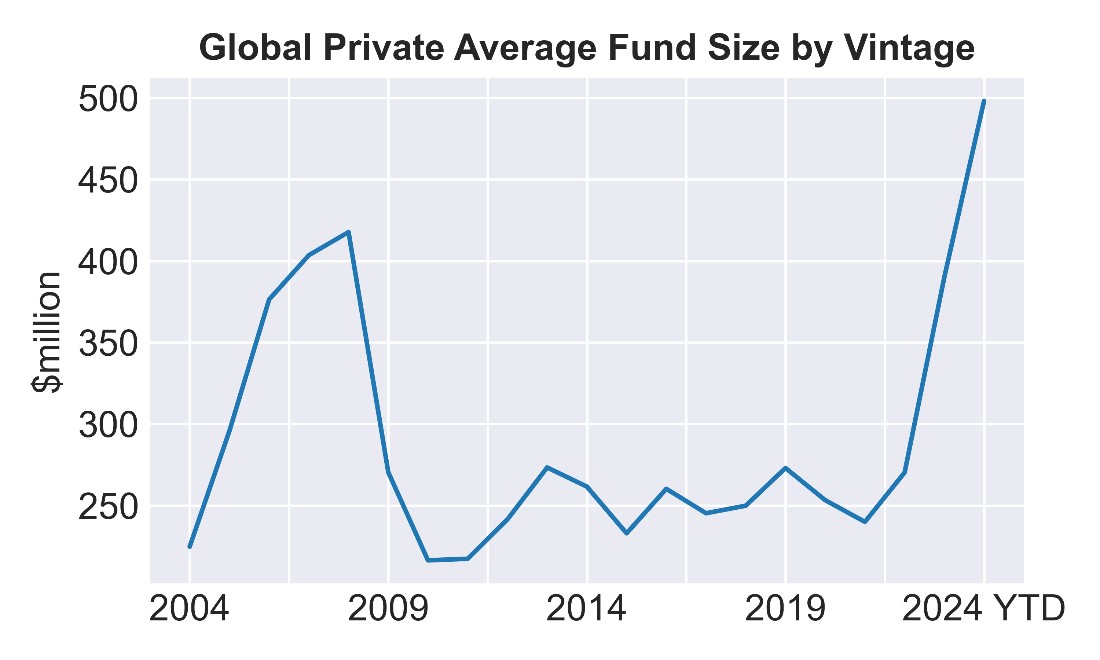

Source: Prequin.

- Dollars raised are flowing to a narrower set of sponsors that have a demonstrated track record of delivering returns over the long run.

- The number of sponsors that raised PE funds in Q1 was roughly cut in half from a year ago, according Pitchbook.

- Not surprisingly, average fund size is moving up, consistent with rising sponsor concentration.

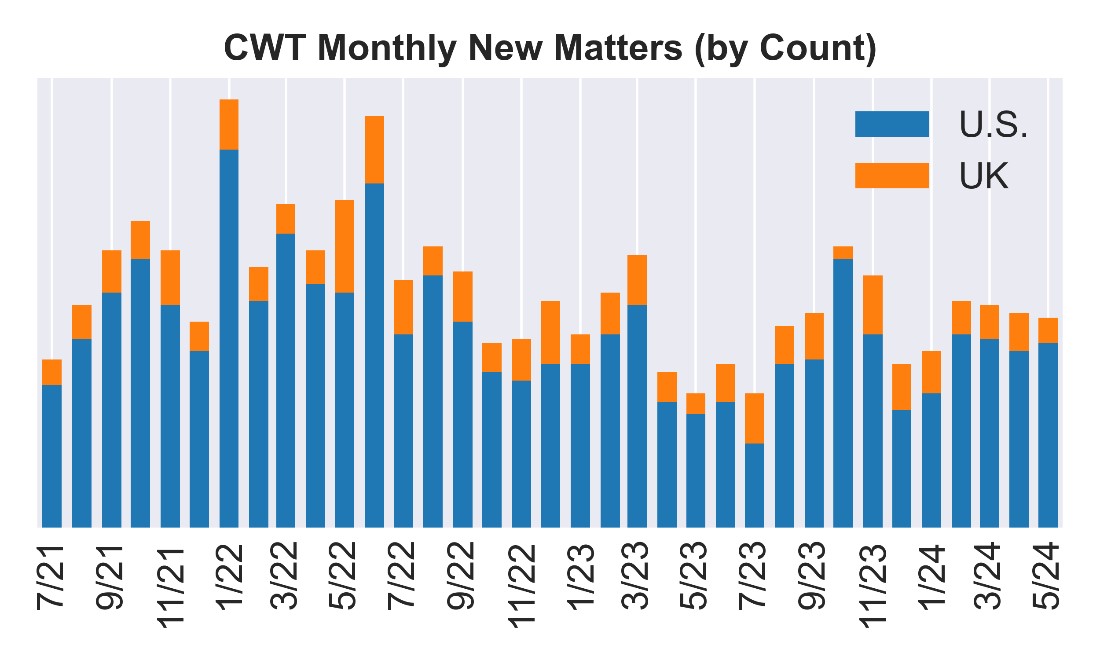

Source: Cadwalader, Wickersham & Taft LLP.

- We kicked off 50 new fund finance representations in May, (U.S. and UK combined), up about 60% from a year earlier.

- Year-over-year gains have been easy to come by in the past two months, given the sharp slowdown in Q2 of last year.

- Despite the narrowing of sponsors apparent in fundraising, we see more lenders involved in the fund finance market YTD and a reduced concentration among the top lenders.

Banks and the Availability of Credit

Source: Federal Reserve Cadwalader, Wickersham & Taft LLP.

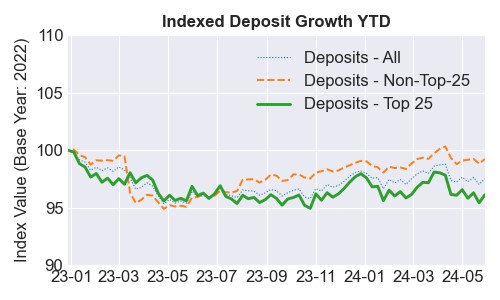

- After significant outflows, deposit levels in the U.S. have been stabilized.

- Below the surface, deposit stability has come at a price: Banks paying more on deposits, backfilling with other borrowing sources, and by using brokered and listed deposits.

- The resulting increase in liability costs continues to pose a headwind to NII and profitability, and some institutions have responded by reducing earning assets.

- For fund finance this has meant divergence between lenders, and generally a more targeted approach on the lender side.

Source: Federal Reserve Cadwalader, Wickersham & Taft LLP.

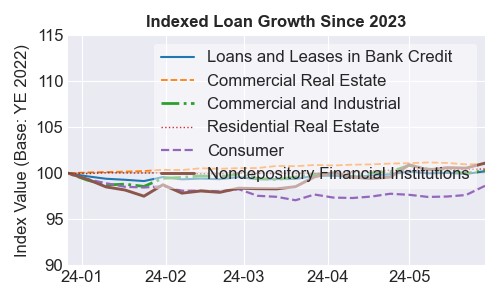

- Overall loan growth has been essentially flat to date in 2024.

- Redeploying the balance sheet in a higher rate environment is running into weak demand in most lending categories and an evolving credit picture. Credit card and auto delinquencies have been moving noticeably higher.

- Not surprisingly, banks have been leaning into the non-depository financial institution category, which includes lending to funds, REITs, BDCs, and other finance providers.

- As we have emphasized in the past, collateral values in fund finance (uncalled capital commitments) are far more insulated from higher rates than many asset classes, such as CRE (higher cap rates) or corporate lending (lower coverage ratios).

Source: FDIC and Cadwalader, Wickersham & Taft LLP.

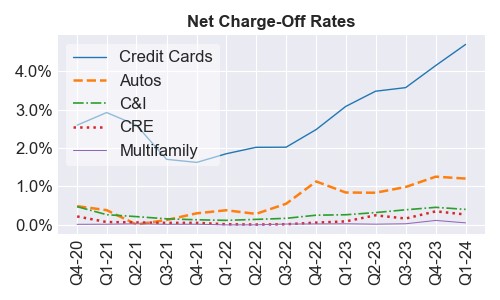

- Charge-offs tend to ramp late in the credit cycle, but credit card and auto loan performance are already showing signs of strain.

- Weakening loan performance in consumer lending categories and the well-publicized challenges in CRE complicate the path to loan growth and balance sheet repositioning.

- But these trends also suggest we could see new lenders legging into fund finance loan participations or standing up new bilateral programs to source loan growth.

Source: Federal Reserve and Cadwalader, Wickersham & Taft LLP.

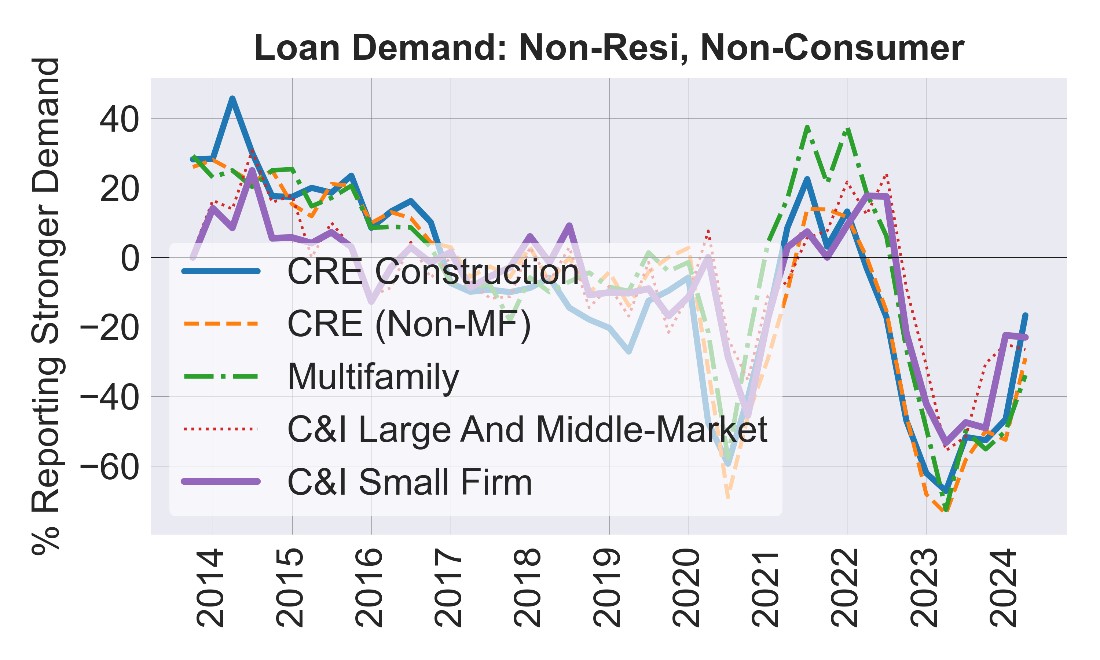

- A higher price of credit has meant lower overall demand for loans.

- On net, bank respondents continue to report weakening demand across lending categories.

- But, outside of consumer loans, where demand is falling, the direction of travel has been up, meaning fewer banks are seeing further weakening in loan demand.

Market Themes

Source: Federal Reserve and Cadwalader, Wickersham & Taft LLP.

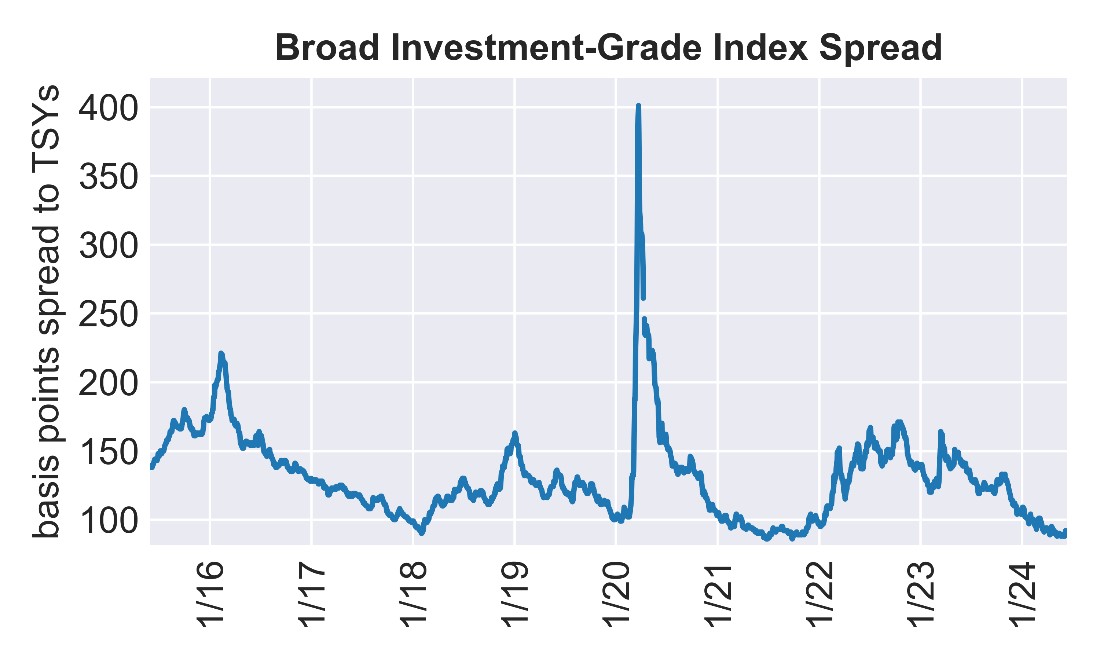

- Outside of fund finance, credit spreads are making a run at post-GFC tights.

- Credit spreads are also increasingly reflecting a reach-for-yield dynamic with lower-investment-grade rated credit products tightening more over the past month.

- In this context, fund finance lending presents a unique value: margins should be intriguing to a broad host of fixed income investors.

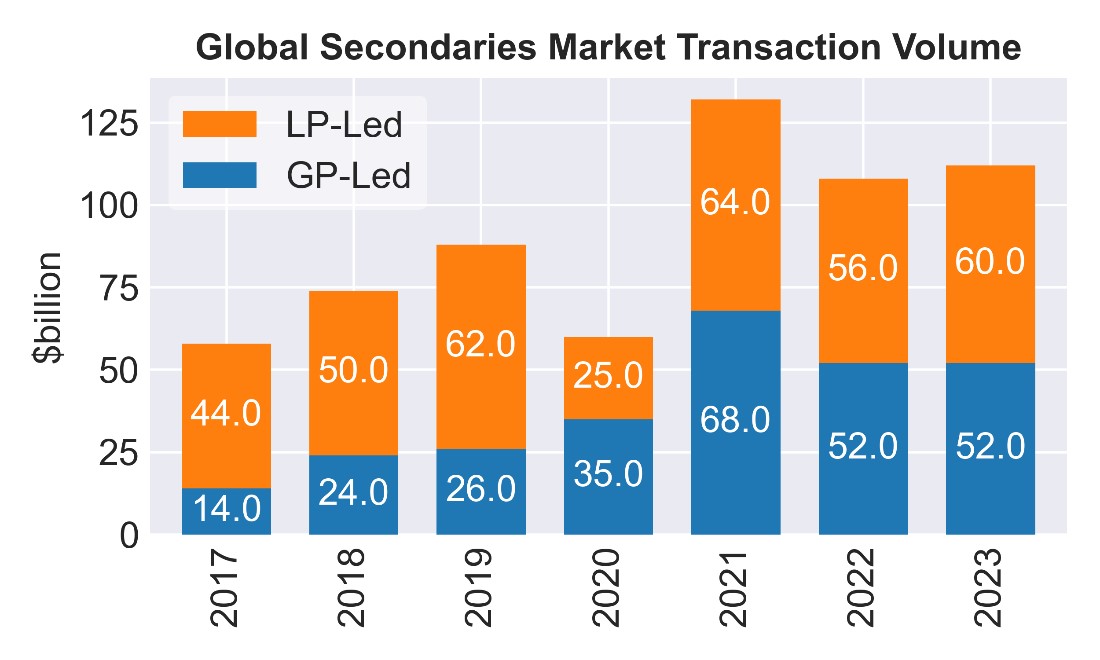

Source: Jefferies LLC.

- The potential for duration lengthening in private fund investments may have been underappreciated coming into 2023-2024.

- As distributions have slowed, investment returns have moved farther into the future, representing a portfolio management challenge for LPs.

- Not surprisingly, LP-led secondaries activity increased in 2023 as LPs sold positions to raise liquidity.

- These conditions could help secondaries volume again in 2024 and, over time, may support NAV origination volume growth.

Not limited to fund finance:

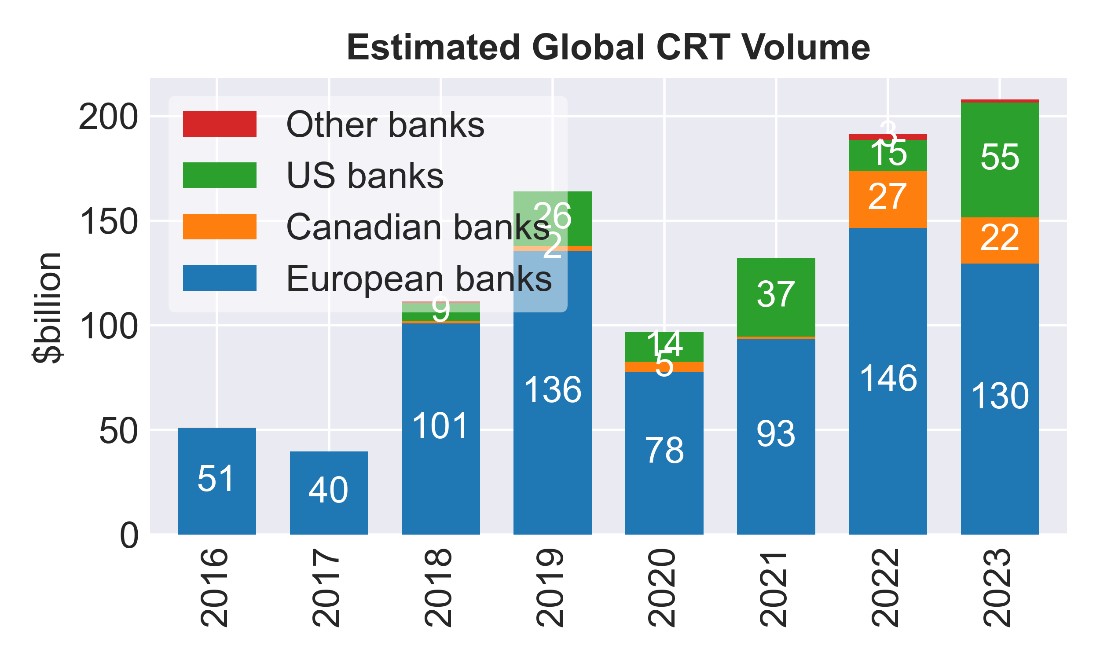

Source: AXA IM Alts and Bloomberg LP.

- More than ever, the fund finance market requires a full platform approach.

- In 2024, we are seeing growing need among lenders for capital management strategies, which brings multiple disciplines into the fund finance conversation.

- CRT/SRT transaction volume continues to gain momentum.

- In Europe, credit ratings are part of the capital management toolkit, but on both sides of the pond, structured transactions and the inclusion of non-bank lenders are real themes. All require a coordinated multi-discipline approach.

Conclusion

We end with a few observations from the first half that we expect will continue to shape the fund finance market in the remainder of the year.

- The NAV market continues to see steady growth, although perhaps not (yet) at the breakneck speed some have predicted. That growth has been accompanied by increased media and investor scrutiny, with certain publications running with the theme that investors object to the use of NAV financing. This criticism has included splashy quotes by a few select investors and has focused largely on the use of NAV financing to distribute capital to investors because of the costs of such financing and the impact such distributions may have in improving DPI numbers. Our experience of the market though has been that NAV financing is being infrequently used to fund distributions (and then only based on the needs of, and based on input from, investors). We more frequently see such financing used to make strategic acquisitions, to support struggling portfolio companies or to refinance higher cost corporate debt, all of which should be accretive to fund investors. For these use cases, we see robust investor support and acceptance.

- Insurance money is king. Insurance money has come to permeate the fund finance market like never before. This is evident in the market as many asset managers have set up funds dedicated to deploying insurance company money into fund finance deals. Facilities are incorporating term tranches into what have historically been revolving structures. Term loans are subjected to non-call periods. And rating agencies are developing frameworks to rate both sublines and NAV loans. All of this is being done to attract money from the insurance sector, with insurance companies willing to provide financing to top tier managers and diversified portfolios for longer terms and at lower cost. This has attracted the attention of the NAIC, which has a lead role in setting regulatory and capital standards for U.S. insurance companies. Market participants are watching to see how recent guidance regarding what constitutes a bond will be implemented.

- In the U.S., the regulatory capital rulemaking process is expected to move forward in the coming months, and could begin to inform the balance sheet allocation and facility pricing.

- Securitization techniques are increasingly being deployed in the fund finance world. Collateralized fund obligations, rated note feeders and other A/B structures have become a regular feature of fund finance borrowers and structures.

- Earlier in the year we pointed out that more granular call report disclosure on loans to non-depository financial institutions (NDFIs) signaled coming regulatory attention to this lending category going forward. The Federal Reserve demonstrated its building interest in two important ways this week: Early in the week, the Federal Reserve Bank of New York published a three-part series on nonbank financial institutions. Then, yesterday, the Fed Board of Governors proposed revisions to its Capital Assessments and Stress Testing information collection forms (FR Y-14) that cites concerns over the rapid growth of bank exposures to NDFIs and the associated risk to banks. The proposed form update requires filers to disclose more information on NDFI loans that will cover the type of entity, security, fee structure, and borrower financial information. These disclosures are aimed at addressing a “material data gap” in the stress test process.

- Similarly, earlier this year the Bank of England’s Prudential Regulatory Authority (PRA) issued a letter to bank chief risk officers detailing findings from its ‘thematic review of private equity related financing activities’. The PRA specifically referred to the increase in bank exposure to what it calls ‘non-traditional’ forms of financing to PE funds, namely subscription and NAV facilities, and identified weaknesses in the current risk management frameworks that banks employ in order to control their exposure to the PE sector. Expect closer regulatory attention to be a prominent part of the operating environment going forward.

- Given the theme of balance sheet repositioning, lender networking really matters—the next new deal may be coming from a lender hand-off. Syndication desks and industry relationships are more important than ever.

- So is innovation. We keep adding to the toolkit – LP liquidity, lender capital management, and capital markets are key themes that are driving future innovation and suggest thinking broadly. Let us know how we can help.