On July 29th, 2021, the Alternative Reference Rate Committee (“ARRC”) formally recommended the adoption of CME Group’s forward-looking Secured Overnight Financing Rate term rates (“Term SOFR”).1 This announcement completes the transition plan ARRC has been working towards since 2017 and provides market participants with the tools they need in order to transition from LIBOR to SOFR according to Tom Wipf, the ARRC Chairman.

There is no doubt that the formal recommendation of Term SOFR is a significant step in the transition away from LIBOR. ARRC has recommended Term SOFR as the primary fallback option in the LIBOR replacement waterfall since the ARRC hardwired approach made its original debut in April 2019, and as a result Term SOFR has been incorporated into a significant portion of new debt issuances.2 Adoption of Term SOFR allows for an easier transition from LIBOR in bilateral and syndicated loan markets because it operates similarly to LIBOR and allows Borrowers to have certainty over short term borrowing costs.

However, ARRC’s view that market participants have all of the information they need to finalize the transition away from LIBOR assumes that markets will enthusiastically accept SOFR as LIBOR’s only replacement. SOFR, which is considered a risk-free rate because it is based on underlying transactions that are secured by US Treasury securities, does not contain a credit risk component. This is different from LIBOR which was based on unsecured inter-bank lending transactions and thus did reflect an element of credit risk.

In recent months some market participants have questioned whether SOFR is an appropriate reference rate for all previously LIBOR-based transactions. Because LIBOR contained an element of credit risk, as lenders’ cost of funding increased LIBOR would also increase. However, the same may not be true of SOFR which could actually decline in times of economic distress as the Federal Reserve pushes rates on US Treasury securities down to stimulate the economy. Consequently, some market participants fear a scenario where lenders are facing increases to their costs of funds while at the same time the return they are receiving on SOFR-based loans is decreasing resulting in an unintended transfer of value from lenders to borrowers.

As a result of these concerns surrounding SOFR, several alternative credit sensitive rates that have more closely tracked LIBOR historically have received significant attention from both government actors and market participants. In February, the Federal Reserve System, the Federal Deposit Insurance Corporation and the Office of the Comptroller of the Currency convened a series of workshops to explore credit-sensitive rates as alternative replacements to LIBOR.3 Additionally, the Loan Syndications and Trading Association published a rider to the ARRC hardwired fall back language that contemplates the selection of a credit sensitive rate in lieu of a SOFR-based rate, and the International Swaps and Derivatives Association (“ISDA”) modified its definitions to accommodate certain credit sensitive rates.45

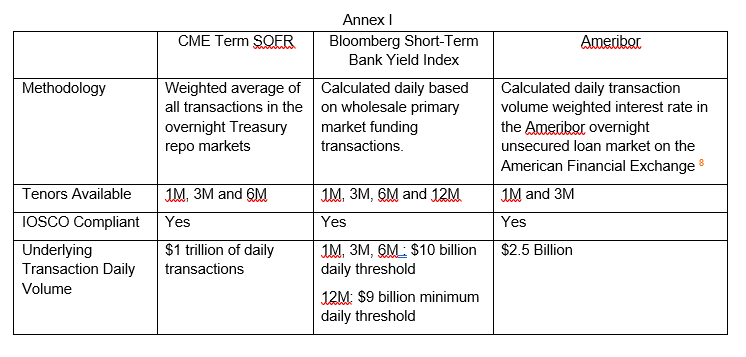

The primary credit sensitive rates generating significant buzz in the market currently are the Bloomberg Short-Term Bank Yield Index (“BSBY”) and Ameribor which are both briefly summarized on Annex I hereto.6 Ameribor was originally created to reflect the cost of borrowing for smaller lenders in the United States and currently has banks in all 50 states participating. BSBY seeks to provide a rate that works for all banking institutions by including index transactions that are anchored in commercial paper, certificates of deposit, U.S. dollar bank deposits and short term bank bond trades.

In response to the increased market interest in credit sensitive rates and BSBY in particular, the chair of the U.S. Securities and Exchange Commission, Gary Gensler, expressed concerns over the similarities between BSBY and LIBOR which he felt could result in the same issues that lead to LIBOR’s ultimate demise. He noted that the 34 panel banks that BSBY draws from is not materially better than the 11 to 16 banks upon which LIBOR is currently based. He also believed that low underlying trading volumes upon which BSBY is based could create the same perverse incentives that led to manipulation of LIBOR because of a relatively small number of transactions backing the potentially hundreds of trillions of dollars of financial instruments currently liked to LIBOR. Finally, he was concerned about BSBY’s ability to continue during a crisis, citing the beginning of the COVID-19 pandemic where the commercial paper market vanished for a short period of time. Similar concerns exist for Ameribor – given the low trading volumes and the fact that the transactions that back Ameribor are primarily between small and regional institutions, Ameribor rates may not reflect rates that one would see in capital market transactions or other transactions among larger financial institutions.

Despite the detractors, Ameribor and BSBY have supporters and undeniable benefits. Ameribor is a rate that regional and community banks can use to align their costs of funds given that lenders often don’t have access to the secured overnight repo markets represented by SOFR. With regard to BSBY, Bloomberg published a report that addresses a number of the concerns raised by Mr. Gensler. Particularly, the report notes that while SOFR will most likely be the primary reference rate for derivatives, floating rate notes, consumer loans and securitizations, Bloomberg says that the majority of credit sensitive rate use cases are for commercial and business loans that make up about $6.2 trillion of the existing $220 trillion market for LIBOR-linked financial instruments. Bloomberg argues that for this market segment, the number of transactions underlying BSBY is sufficient.7 Further, Bloomberg addresses the potential for manipulation of BSBY by saying that the money markets underpinning BSBY are composed of buyers and sellers with competing interests and that attempts to manipulate BSBY could lead to significant losses, neither of which are the case for LIBOR.

One thing is clear – while the ARRC announcement provides the final details on what a transition to SOFR should look like, it does not necessarily mean that a transition to SOFR for all products is certain.

1In approving an administrator of Term SOFR, ARRC went through a process that began in March 2021 with a request for proposal. Following a thorough evaluation process, ARRC selected CME Group. ARRC used the following principles to choose a Term SOFR administrator: (a) the rate must meet the ARRC criteria for an alternative reference rate; (b) the rate must be rooted in a robust and sustainable base of derivatives transactions over time and (c) the rate must have a limited scope of use.

2In June 2021, close to 90% of new issued syndicated term loans used the ARRC recommended hardwired approach according to Covenant Review. Additionally, ARRC noted that in February 2021, more than 56% of newly issued institutional loans utilized ARRC’s hardwired approach.

3Federal agencies have generally taken the position that they do not support one rate over another and that each market participant should choose the rates that meet such participant’s needs.

4You can find the LSTA Rider at: https://www.lsta.org/content/csr-slot-in-rider-for-fallback-language-market-advisory/

5Covenant Review has reported that up to 21% of the newly issues syndicated institutional loans in May and June included the credit sensitive rate rider from the LSTA.

6There are other credit sensitive rates that have been developed by certain market participants including the ICE Bank Yield Index, the HIS Markit Credit Inclusive Term Rate/Spread and the Tradeweb/IBA constant maturity Treasury Rate.

7As of publication of July 1, 20220, Bloomberg said the three day average transaction volume for BSBY was $200 billion. https://assets.bbhub.io/professional/sites/10/Bloomberg_BSBY_Report_070121.pdf