[co-author: April Breyer Menon]

Introduction

It has been 13 years since the Biologics Price Competition and Innovation Act (BPCIA) was enacted and biosimilars had a pathway to enter the U.S. market. While there have been challenges over this time, the U.S. biosimilar market has come a long way and has overcome many hurdles. We will explore some of the issues biosimilars have faced when entering the U.S. market, with a particular focus on the impact of inter partes reviews (IPRs), post grant reviews (PGRs), and the BPCIA litigation patent dance, as well as challenges to gaining market share after launch.

The Current State of the Biosimilars Industry in the U.S.

There are currently (FN 1) 40 approved biosimilars of 11 reference products in the U.S. market, seven of which were approved in 2022. This is a marked increase over the prior two years, which had seven total approvals due to COVID-19 related approval delays. Thus far, interchangeable approvals have been limited, with only four approved interchangeable biosimilars of three reference products to date, two of which were approved in 2022.

Biosimilar launches picked up starting in 2019, and now 27 biosimilars have reached the market, which is over two-thirds of those approved. There is only one reference product, Enbrel® (etanercept), for which biosimilars have been approved but have not yet launched, due to litigations resulting in injunctions until the time of patent expiry.

The beginning of 2023 saw a much anticipated launch of the first Humira® (adalimumab) biosimilar Amjevita™ (adalimumab-atto), with at least seven additional biosimilars of Humira to launch during the remainder of this year. The first interchangeable biosimilar of Humira, Cyltezo® (adalimumab-abdm) and the first high-concentration adalimumab biosimilar, Hadlima™ (adalimumab-bwwd), are both expected to launch as early as July 1, 2023. The entrance of a high-concentration adalimumab biosimilar is significant, because over 80% of Humira prescriptions are for the high-concentration formulation.

Numerous biosimilar applications are currently pending at the FDA, including applications for reference products that have yet to see an approved biosimilar, including Eylea® (aflibercept), Tysabri® (natalizumab), Actemra® (tocilizumab), Stelara® (ustekinumab), Novolog® (insulin aspart), Humulin® R (human insulin), and Prolia®/Xgeva® (denosumab). As a result, 2023 could see a new wave of biosimilar competition enter the market.

Impact of IPRs, PGRs, and the BPCIA

Patent protection is a significant consideration for biosimilars entering the U.S. market. There are a variety of ways patent disputes proceed in the U.S., including IPRs and PGRs at the patent office, and litigation under the BPCIA, often referred to as the “patent dance,” where biosimilar manufacturers and reference product sponsors (RPSs) exchange patent validity and infringement information prior to filing a lawsuit in district court. All of these mechanisms have the goal of an early resolution of patent disputes prior to biosimilars coming on the market.

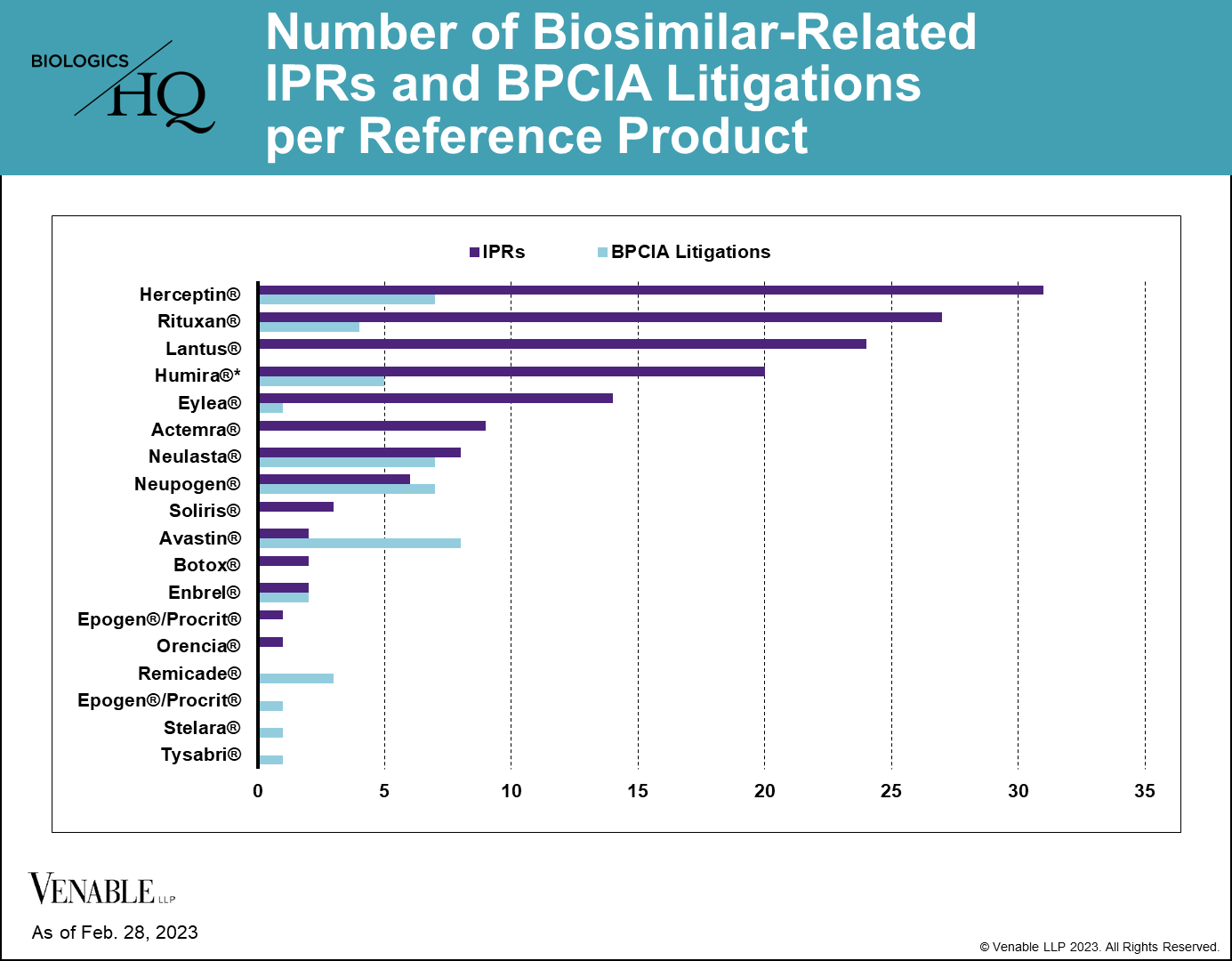

As of February 28, 2023, there have been 144 biosimilar-related (FN 2) IPRs encompassing 70 patents and 14 reference products, and there have been 46 BPCIA litigations related to 12 reference products. PGRs have not been a preferred way of resolving biosimilar-related patent disputes, with only three biosimilar-related PGR filings to date. While most of the RPSs have faced both IPRs and litigations related to their patents, some biologic patents have only faced one type of challenge, which can be seen in the graph below.

Figure 2: One litigation is counted twice as it related to patents covering both Neupogen and Neulasta. While Lantus patents have been subject to litigation, none of those litigations were under the BPCIA and thus are not included.

Each biosimilar is reaching the market through a different path, be it through IPRs, litigations, settlements, or a combination of these. As such, we reviewed the patent disputes at the patent office (IPRs and PGRs) and in district court for each biologic and biosimilar to understand the overall outcomes and identify any noteworthy trends.

We found that a relatively small number of biologic patents have been invalidated with respect to any individual biologic, that IPRs can be effective ways of avoiding litigation, and that the BPCIA dispute resolution process has not been a significant barrier for many biosimilars.

The Number of Patents Initially Asserted in a BPCIA Litigation Could Affect Its Resolution

Reviewing the BPCIA litigations to date, we found that the number of patents asserted could play a role in the resolution of the litigation. 21 of the 46 (45.7%) BPCIA litigations involved five or fewer patents, 20 (43.5%) involved more than 10 patents, and 16 (34.8%) involved between 20 and 60 patents.

Of the cases that have gone to resolution of either a jury/bench trial verdict or summary judgment, all of them involved five or fewer patents. In contrast, no cases that began with more than five patents proceeded to a resolution by the court on infringement or validity.

Of the nine cases reaching resolutions through a jury/bench trial verdict, summary judgment, or stipulated judgment, three were resolved in favor of the RPS, and the remaining six were resolved in favor of the biosimilar, all of which were resolved by determining the biosimilar did not infringe the patents at issue. Only four of the 46 (8.7%) cases were resolved at trial (one jury verdict and three bench trials), with biosimilars and RPSs each winning half of the cases.

While there can be many reasons parties decide to settle, the risks of an adverse judgment, as well as the expense in cases involving large numbers of patents are significant for both sides.

In Litigation, Biosimilars Have Prevailed Through Proving Non-Infringement, Not by Invalidating Patents

There have been nine BPCIA cases involving five reference products that have concluded with infringement and/or validity determinations by the court (7), or through stipulated judgments of non-infringement by the parties (2). In these cases, three were resolved in the RPS’s favor with resulting damages (1) and permanent injunctions (2), and the remaining six resulted in a finding that the patents remaining at issue were not infringed by the biosimilar.

The fact that the favorable outcomes for biosimilars typically did not find patents invalid is interesting, particularly because some have suggested that so-called weak drug patents are keeping biosimilars off the market. That hasn’t proven to be true in the BPCIA litigation context based on the outcomes.

Few Biologic Patents Have Been Invalidated in Biosimilar-Related IPRs for Any Given Reference Product

40 of 62 (64.5%) patents subject to a terminated biosimilar-related IPR survived without cancellation of a single claim. 22 of 62 (35.5%) patents had at least some claims invalidated or disclaimed, related to nine reference products. Of those 22 patents, there were two disclaimers, two patents lost some challenged claims but not all in final written decisions (FWDs), 12 patents were lost in their entirety in FWDs, and six patents lost all challenged claims in FWDs, but maintained the claims that were not challenged in the IPRs.

Figure 4: Biosimilar-related IPR outcomes by petition and by patent. IPRs that are still pending are not included. Settled / Terminated includes IPRs that were settled or terminated at the Petitioner’s request prior to a final written decision, and include IPRs terminated before and after institution decisions. Claims Cancelled refer to IPRs where the Patent Owner requested cancellation of the challenged claims at any point during the IPR. For patents with multiple IPRs having different outcomes, the outcome at the most advanced stage of the IPR is listed (for example, if one IPR on a patent was not instituted but another IPR on the same patent resulted in a FWD, it is listed as a FWD), and the IPR with the most adverse decision to the patent claims is listed (for example, if one FWD found claims not unpatentable and another FWD found the same claims unpatentable, it is listed as unpatentable). Appeal decisions were considered in the outcomes listed.

Despite some reference products having 20 or more IPRs, we found that few patents have ultimately been invalidated covering any individual reference product. Half (7 of 14) of the reference products having patents challenged in IPRs have not lost a single patent claim. For most biologics that lost patents in IPRs, only 1-5 patents were lost from their estates. For Lantus® (insulin glargine) four patents were invalidated in their entirety and some claims were invalidated in four additional patents (three of the four lost all of the claims challenged in IPRs, but maintained the claims that were not challenged).

Figure 5: Outcomes of terminated biosimilar-related IPRs by patent. Patents with no claims invalidated include those that were not instituted, as well as those with IPRs that were terminated without a final written decision. Patents with at least some claims invalidated include patents where claims were disclaimed by the Patent Owner, and patents where some or all of the challenged claims were invalidated in a FWD. Appeal decisions were considered in the outcomes listed.

Although losing patents in IPRs can potentially be damaging to maintaining a reference product’s market exclusivity, most biologics are covered by multiple patents and are retaining some patent coverage after IPR decisions.

For biosimilars, filing an early IPR petition could result in a settlement with a known launch date early on in development. These early settlements can provide certainty to the innovator and the biosimilar and avoid the expense of a large litigation. So far, RPSs have generally waited to see if an IPR will be instituted prior to settling, with four IPRs settled prior to institution and 20 settled after.

At-Risk Biosimilar Launches Have Been Common and Have Not Ended Up Being So Risky

While at least 11 of the 27 launched biosimilars (40.7%) launched at-risk to at least some degree, so far, none of them have been ordered to pay any damages. While there has been one BPCIA litigation resulting in a damages award, that dealt with pre-launch manufacturing batches that were not found to be covered by 35 U.S.C. § 271(e)’s safe harbor and was not the result of an at-risk launch into the U.S. market.

Some of the at-risk launches took place after an initial decision in the biosimilar’s favor, but before appeals were exhausted, but some took place earlier in litigation. Ultimately, at-risk launches eventually resulted in settlements in most cases.

IPRs Can Be a Successful Way to Avoid Litigation

IPRs have been touted as a less expensive alternative to litigation, and while some may disagree, especially if their patents have been involved in concurrent IPRs and litigation, there is evidence that IPRs can help to avoid resource intensive litigation for biosimilars.

To date, seven biosimilars of six reference products have successfully negotiated settlements after bringing IPRs, prior to any litigation being filed. This includes the Humira biosimilar Yusimry™, Neulasta® (pegfilgrastim) biosimilars Stimufend® and Fylnetra™, Rituxan® (rituximab) biosimilar Ruxience®, Herceptin® (trastuzumab) biosimilar Ogivri®, Soliris® (eculizumab) proposed biosimilar ABP 959 (not yet approved), and Actemra® (tocilizumab) proposed biosimilar MSB11456 (not yet approved).

Some Biosimilars Are Avoiding Costly Patent Disputes Altogether

While IPRs are a potential way to bring about an early resolution to patent disputes, some biosimilars have avoided patent disputes altogether by settling prior to the filing of any IPRs or litigations in the U.S. So far, there have been at least nine biosimilar settlements without a patent dispute in the patent office or district court, including Humira biosimilars Hadlima, Abrilada™, Hulio®, Idacio®, and Yuflyma™, Lucentis® (ranibizumab) biosimilars Byooviz™ and Cimerli™, Rituxan biosimilar Riabni™, and Avastin® (bevacizumab) biosimilar Vegzelma®. There have been two additional biosimilar launches without patent disputes or announcement of a settlement agreement, including Avastin biosimilar Alymsys® and Remicade® (infliximab) biosimilar Avsola®.

It is possible that some of these biosimilars began the patent dance and negotiated settlements during the process, which is a benefit to the early back-and-forth between the RPS and biosimilar manufacturer, and potentially has led to deals between these companies that has kept them out of court.

Overall, 18 biosimilars have launched or negotiated a future launch without a litigation. One company in particular, Fresenius Kabi, has negotiated settlements for all of its three approved or pending biosimilars (Stimufend, MSB11456, and Idacio) without facing a litigation in the U.S.

Other Issues Impacting Settlement Agreements

It should be noted that the U.S. market is not the only location being taken into consideration by RPSs and biosimilar manufacturers when determining the best way to proceed when asserting patents and launching drugs. Some biosimilar settlement agreements have been global, settling disputes and outlining launches around the world, like Mylan and Genentech’s 2017 global settlement agreement for Ogivri, a biosimilar of Genentech’s Herceptin, and Pfizer and Genentech’s 2019 global settlement agreement for Zirabev® (bevacizumab-bvzr), a biosimilar of Genentech’s Avastin.

Since many of the companies in the field have numerous reference products and biosimilars to consider, some settlement agreements have even involved multiple products. For example, a multi-product agreement in July 2020 settled disputes relating to Mvasi® (bevacizumab-awwb), a biosimilar of Genentech’s Avastin and Kanjinti® (trastuzumab-anns), a biosimilar of Genentech’s Herceptin. The settlement followed Mvasi and Kanjinti’s at-risk launches, which took place after the Federal Circuit affirmed district court denials of motions for preliminary injunctions and temporary restraining orders to prevent their launches.

Market Uptake Successes and Challenges

Just like few biosimilar pathways through patent disputes and resolutions have proceeded in the same manner, biosimilars each face a set of unique challenges when attempting to gain market share after entering the U.S. market. Whether it is being the first biosimilar to market, dealing with physician hesitance to prescribe, securing a favorable spot on a formulary, or dealing with multiple competitors, biosimilars have faced challenges to now account for approximately one quarter of the market for those biologics that face biosimilar competition.

The first biosimilar, Zarxio® (filgrastim-sndz), a biosimilar of Neupogen® (filgrastim), was launched in the U.S. in September 2015. In the 7.5 years since, biosimilars have made significant strides in capturing U.S. market share, but success thus far has varied, depending on the type of disease the drug treats, provider preferences, payer coverage, and actions of the RPSs after biosimilar launch.

According to a 2022 report, biosimilars have gained anywhere from 38% to 82% of their respective market shares, with the top market shares of around 80% being for biosimilars of Neupogen, Herceptin, and Avastin, and the lowest market shares of around 40% for biosimilars of Neulasta, Epogen®/Procrit® (epoetin alfa), and Remicade. (FN 3)

While one may expect the length of time on the market would impact the market share taken by biosimilars, this does not appear to be the main driver, as infliximab, epoetin alfa, and pegfilgrastim biosimilars have been on the market for some of the longest time periods, but account for some of the lowest market shares.

It appears from the data that the type of drug, and doctors’ hesitation about prescribing a biosimilar for that particular specialty, may impact uptake in the U.S. market. A January 2023 report from IQVIA Institute, analyzing biosimilar market share in the first three years on the market, shows that oncology biosimilars have gained market share the most quickly, with bevacizumab, trastuzumab, and rituximab biosimilars capturing approximately 70-80% (FN 4) market share within this time period. In contrast, the rheumatology infliximab biosimilars accounted for just over 10% of the market within the same time period. Insulin biosimilars lie somewhere in between, having captured a little less than 30% of the market (FN 5) (when including Basaglar®, which was approved as a “follow-on” biologic, not a biosimilar).

According to a 2022 Cardinal Health report based on physician surveys, doctors in different specialty areas have varying attitudes and hesitations toward prescribing biosimilars, which may account for some of the variation in market shares. The surveys showed that oncologists are more likely to prescribe a biosimilar to new patients (67% vs. 42%) compared to rheumatologists, and oncologists are far more likely to switch a patient having success on a reference product to a biosimilar than rheumatologists (67% vs. 11%). (FN 6)

The differing opinions on biosimilars could have many underlying factors, such as a physician’s prior experience with biosimilars, the type of disease they are treating, the characteristics of the specific patient being treated, the length of time the patient will be on the drug, and cost to the provider and patient. However, at this time, physicians across specialty areas have said that they are at least somewhat familiar with biosimilars, with the majority being comfortable with the FDA’s biosimilar approval process and prescribing biosimilars. (FN 7)

Insurance coverage by placing a biosimilar on the formulary has been a big driver for biosimilar uptake. In fact, Cardinal Health found a 97% correlation between biosimilar uptake and coverage of biosimilars by insurance plans at parity to or in preferred formulary tiers compared to the reference product when analyzing Rituxan biosimilars. (FN 8) From December 2019 through September 2021, the rate of rituximab biosimilar adoption rose at a similar rate to the increasing number of patients whose insurance covered the biosimilars. (FN 9)

Cost savings to patients is another factor driving prescriptions of biosimilars. Physicians across specialty areas surveyed by Cardinal Health agreed that cost savings to their patients and insurance payer coverage are important factors when considering treatment options. (FN 10) But, many providers do not see enough of a cost benefit to switch patients to biosimilars. (FN 11) Whether a patient will see any cost savings can be difficult for providers to know, as there are many different payers and levels of coverage that can be challenging to navigate. It is also difficult to know whether savings for biosimilars are being seen by the patient, or whether the savings is mainly going to middlemen like pharmacy benefit managers. (FN 12) Insurance company mandates may be one way to increase biosimilar usage, as physicians have indicated they would be likely to prescribe a biosimilar if the patient’s insurance mandated it. (FN 13)

Payer coverage for biosimilars has been improving and increased significantly between the end of 2019 and the end of 2021, leading many biosimilars to have better coverage scores (FN 14) than their reference products. (FN 15) The increase in coverage may contribute to increased usage of biosimilars, as there does seem to be a correlation between payer coverage and market share. Biosimilars that had better payer coverage scores than their reference products tended to have higher market share than biosimilars where the reference product had better coverage. According to Cardinal Health, biosimilars of rituximab, bevacizumab, trastuzumab, and filgrastim, all had better coverage scores at the end of 2021 than their reference product, and these were the biosimilars with the highest market share at that time period. (FN 16) In contrast, biosimilars of pegfilgrastim, and insulin glargine had less favorable coverage, and all had gained less market share. (FN 17)

Another factor at play in biosimilar uptake may be related to the response of a reference product sponsor to biosimilar competition. IQVIA found that when originator drugs respond to biosimilar competition by lowering their prices more drastically, the biosimilars did not gain as much market share. (FN 18) For example, the Neulasta average sales price (ASP) decreased by 66% after biosimilar competition, and the reference product sales volume decreased by 36%. (FN 19) In contrast, the Neupogen sales price rose by 3% after biosimilar competition entered the market, and the reference product sales volume decreased by 86%. (FN 20)

IQVIA data suggested that the cost savings from some of the biosimilars with the highest uptake may also have led to their achieving higher market shares. In particular, the oncology drugs bevacizumab, rituximab, and trastuzumab, that have all seen high levels of biosimilar uptake, had a high cost of treatment (approximately $4,500 to $8,500 for the originator prior to biosimilar competition) and large biosimilar discounts of over 50%, leading to large savings by using a biosimilar. (FN 21)

An additional factor that can complicate uptake is the way a particular biologic is distributed. A biosimilar can either be acquired and distributed by pharmacies, which are subject to pharmacy benefit plans (called “white-bagging”), or they can be acquired and distributed by the providers (called “buy-and-bill”), which may give the providers benefits such as high reimbursements compared to their costs to acquire the drugs. IQVIA found that in the buy-and-bill context, biosimilars on average had significantly higher uptake compared to when they were white-bagged, with 31% vs. 8% uptake at six months and 57% vs. 35% uptake after two years. (FN 22)

As interchangeable biosimilars are becoming available, it will be interesting to see whether the designation helps those products to see increased market share. In a survey of physicians’ attitudes toward adalimumab biosimilars, over 60% of doctors practicing dermatology, rheumatology, and gastroenterology indicated that they will only feel comfortable prescribing an adalimumab biosimilar if it has an interchangeable designation. (FN 23) A survey of ophthalmologists indicated that 56% will only feel comfortable prescribing a biosimilar if it has an interchangeability designation. (FN 24) Based on these surveys, it seems that achieving an interchangeability designation could have a significant impact on some of the newest biosimilars generating a large market share.

Conclusion

Biosimilar manufacturers have faced challenges to develop, market, and sell their drugs in the U.S. So far, the outcomes have been product specific, with some reaching the market without the expense of IPRs and litigation, and others facing numerous patent disputes and injunctions impacting their market entry. Some biosimilars have managed to overtake reference product market shares, while others have struggled to gain footing.

Footnotes

1 Statistics in this article are through February 28, 2023.

2 We define “biosimilar-related” patent disputes as those involving drug companies that have an approved biosimilar of the reference product or one in development at the time the dispute was filed.

3 See Amgen Biosimilars “2022 Trends in Biosimilars Report Preview” at Figure 6, available at: https://www.amgenbiosimilars.com/commitment/2022-Biosimilar-Trends-Report.

4 See IQVIA Institute “Biosimilars in the United States 2023-2027, Competition, Savings, and Sustainability” at Exhibit 9, available at: https://www.iqvia.com/insights/the-iqvia-institute/reports/biosimilars-in-the-united-states-2023-2027.

5 See IQVIA Report at Exhibit 14.

6 See Cardinal Health “2022 Biosimilars Report: The U.S. Journey and Path Ahead,” at Figure 6, available at: https://www.cardinalhealth.com/content/dam/corp/web/documents/Report/cardinal-health-2022-biosimilars-report.pdf.

7 See Cardinal Health 2022 Report at Figures 5, 11, 12, and 30; see Cardinal Health “2023 Biosimilars Report: Tracking market expansion and sustainability amidst a shifting industry,” at Figures 4, 7, 15, available at: https://www.cardinalhealth.com/content/dam/corp/web/documents/Report/cardinal-health-biosimilars-report-2023.pdf.

8 See Cardinal Health 2022 Report at Figure 42.

9 See Cardinal Health 2022 Report at Figure 42.

10 See Cardinal Health 2022 Report at pg. 26-27, 32, 38, 44; see Cardinal Health 2023 Report at Figure 40.

11 See Cardinal Health 2023 Report at Figure 13.

12 See Cardinal Health 2022 Report at pg. 24.

13 See Cardinal Health 2023 Report at Figures 8, 16, 25.

14 “Coverage scores” were calculated by Cardinal Health by reviewing the spectrum of coverage on payer formularies and medical policies and scoring them from 1 (worst coverage available – with no product or unknown product coverage) to 6 (best coverage available – with full product coverage and no step therapy requirements). See Cardinal Health 2022 Report at pg. 48.

15 See Cardinal 2022 Health Report at pg. 48-50, 52-53.

16 See Cardinal 2022 Health Report at pg. 15, 48-50.

17 See Cardinal 2022 Health Report at pg. 15, 52-53.

18 See IQVIA Report at Exhibit 19.

19 See IQVIA Report at Exhibit 19.

20 See IQVIA Report at Exhibit 19.

21 See IQVIA Report at Exhibit 18.

22 See IQVIA Report at Exhibit 11.

23 See Cardinal Health 2023 Report at Figure 38.

24 See Cardinal Health 2023 Report at Figure 53.